USD

USD GBP

GBP CNY

CNY EUR

EUR INR

INR JPY

JPY MYR

MYR ZAR

ZAR KRW

KRW THB

THBThe Transformation of the American Hospital, Assessment to 2020

The Transformation of the American Hospital, Assessment to 2020

Focus Shifts from Patient Volumes to Value-based Outcomes and Collaborative Care

04-May-2016

North America

$4,950.00

Special Price $3,712.50 save 25 %

Description

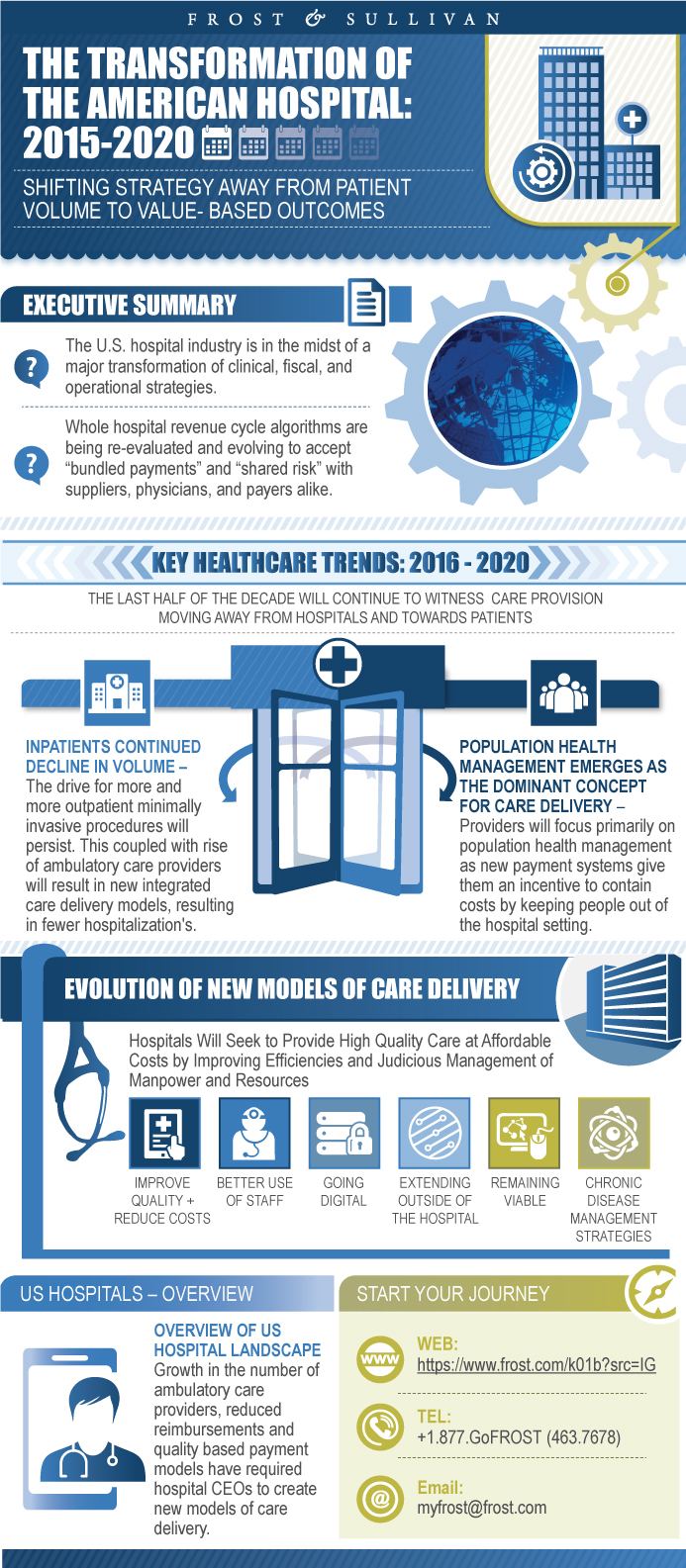

The US hospital industry is in the midst of a major transformation of clinical and operational strategy, moving from a “heads to beds” provider-centric delivery system to a collaborative care continuum, with the patient at the epicenter of attention. Research analysis covers how reimbursement cuts and regulatory changes contribute towards the evolving role of hospital-based care in the United States. It examines the current financial status of US hospitals; the emerging partnership models between hospitals and ambulatory care providers; and the decentralization of diagnostic imaging and clinical laboratory services from within hospitals to free-standing service providers. A vision of care provision in 2020 and beyond ends the study.

RESEARCH: INFOGRAPHIC

This infographic presents a brief overview of the research, and highlights the key topics discussed in it.Click image to view it in full size

Table of Contents

Evolution of New Models of Care Delivery

Competitor Influence

- Pressure hospitals face

- Moving beyond acute care setting

- Re-structuring for consolidation

Lean Innovations and Management Principals to be Key

- Infrastructure

- Technology

- Financial

- Process Management

- People

Rise of Smart Hospitals

- Enterprise Connectivity

- Devices and Sensors

- Healthcare IT

Mapping the Transformation of Care Provision

- Assessing the Vendor Opportunity Landscape

Snapshot of Current Status

What Keeps Hospital CEOs Awake at Night

Key Hospital Objectives

Challenges Posed by the Affordable Care Act (ACA)

Financial Status—For-profit Hospitals

Financial Status—Not-for-profit Hospitals

Hospital-owned Insurance Plans

Financial Status—Rural Hospitals

Healthcare Spending Landscape in the United States

Hospital Consolidation Overview

Hospital Services Expansion

Role of ACOs

CMS Stipulations for Medicare ACOs

ACO Quality Measures—4 Key Domains

Role of ACOs in Chronic Disease Management

Accountable Care Organization—Infrastructure Landscape

Accountable Care Organization—Segment Landscape

Accountable Care Organization—Patient Coverage

Accountable Care Organization Model—Analysis

Changing Reimbursement Models

Types of Value-based Payments

Bundled Payments Landscape

Inpatient Landscape by Payor

Hospital Reimbursement Landscape

Medicare Advantage (MA) Plans

Inpatient Statistics Analysis

Hospital Inpatient Volume Trends

Financial Impact of Hospital Consolidations

Outpatient Statistics Analysis

Ambulatory Surgical Center Trends

Ambulatory Care Provider Model 1—Retail Clinics

Future of Retail Clinics

Transition of Retail Clinics

Health Systems Partnerships With Retail Clinics

Ambulatory Care Provider Model 2—Urgent Care Clinics

Health Systems Partnerships With Urgent Care Clinics

Ambulatory Care Provider Model 3—Bridge Clinics

Ambulatory Care Model 4—Virtualization of Primary Care

Ambulatory Care Model 5—Telemedicine in Rural Hospitals

Hospital Revenues by Key Specialties

Clinical Specialty Area 1—Orthopedics

Clinical Specialty Area 2—Cardiovascular Diseases (CVDs)

Clinical Specialty Area 2—Emergence of TAVR

Clinical Specialty Area 2—Emergence of TMVR

Clinical Specialty Area 3—Behavioral Health

Clinical Specialty Area 4—Long-term Care (LTC) Hospitals

Hospital Acquired Infections—A Major Hospital Challenge

Solution for HAIs—CMS Partnership for Patients Program

Personalized Genetic Medicine

Case Studies

3D Printing

Nano Medicine

Summary of Medical Imaging Trends

Technical Reimbursements—Target of Medicare Cuts

Imaging Procedure Landscape

Imaging Centers—Facing a Tough Economic Environment

Joint Ventures—An Attractive New Model of Collaboration

Benefits of Joint Ventures

Replacement of Joint Ventures—Rise of Hybrid Models

Hybrid Partnership Models—Examples

Summary of Clinical Laboratory Trends

Clinical Laboratories in the United States—Snapshot

Clinical Laboratories—Key Specialty Areas of Focus

Decentralization of Clinical Laboratory Testing

Hospitals and Independent Labs—Types of Partnerships

Independent Clinical Labs—Consolidation Trends

Point of Care Testing—The Next Big Thing

Evolution of the Healthcare Landscape: 2010–2020

Key Healthcare Trends: 2016–2020

From Episodic to Managed Care

A Healthcare Utopia—Vision for 2020 and Beyond

Healthcare Innovation will Drive New Market Opportunities

Facilitating Continuum of Care Services

Role of Big Data

Creating Big Data Analytics Solutions

Definitions of Key Terms

Value Proposition: Future of Your Company & Career

Global Perspective

Industry Convergence

360º Research Perspective

Implementation Excellence

Our Blue Ocean Strategy

- 1. Financial Status—For-profit Hospitals

- 2. Median Annual Revenue Growth, United States, 2013–2014

- 3. Median Annual Expenditure Growth, United States, 2012–2014

- 4. Rural Hospital Closures, United States, 2010–Q32015

- 5. Healthcare Spending, United States, 2013

- 6. Healthcare Spending by Payer, United States, 2013

- 7. Hospital Acquisition Deals, United States, 2006–2010

- 8. Hospital Acquisition Deals, United States, 2010–2014

- 9. Growth in ACOs, United States, 2011–Q12015

- 10. Growth in ACO Contracts, United States, 2011–2014

- 11. Breakup of ACOs by Ownership, United States, 2015

- 12. ACO Population Coverage, United States, 2011–2020

- 13. Reduction in Number of Pioneer ACOs, United States, 2012–2014

- 14. Patients Treated in Hospitals by Payer, United States, 2013

- 15. Medicare FFS Payments for Hospital Inpatient & Outpatient Services*, United States, 2005–2013

- 16. Medicare Spending Trends

- 17. Medicare Advantage Enrollees, United States, 2009–2015

- 18. Distribution of Enrollees, United States, 2015

- 19. Inpatient Admissions/1,000 Population, United States, 2005–2013

- 20. Inpatient Surgeries Performed, United States, 2005–2013

- 21. Inpatient Days/1,000 Population, United States, 2005–2013

- 22. Total Inpatient Days, United States, 2005–2013

- 23. Markup of Hospital Charges Above Costs For Medicare Services, United States, 2005–2012

- 24. Top 50 Hospitals in Terms of Markups

- 25. Outpatient Visits/1,000 Population, United States, 2005–2013

- 26. Total Outpatient Visits, United States, 2005–2013

- 27. Total Outpatient Surgeries, United States, 2005–2013

- 28. ASC Growth Trends, United States, 2008–2014

- 29. Number of Retail Clinics, United States, 2009–2021

- 30. Patients Visiting Retail Clinics, United States, 2013–2021

- 31. Retail Clinic Revenues, United States, 2013–2021

- 32. Urgent Care Clinic Ownership, United States, 2015

- 33. Virtual Doctor Consultations*, United States, 2015–2020

- 34. Hospital Revenues by Key Specialties

- 35. Increasing Annual CMS Spending on Hip and Knee Bundles, United States, 2016–2020

- 36. Incidence of Aortic Stenosis, United States, 2015–2025

- 37. Incidence of Severe Mitral Regurgitation, United States, 2015–2025

- 38. Clinical Specialty Area 3—Behavioural Health

- 39. Rising Costs of LTC

- 40. Percentage Split of Medicaid Spending on LTC, United States, 2005–2013

- 41. Clinical Specialty Area 4 - LTC Facilities

- 42. Clinical Specialty Area 4 - Medicare Spending

- 43. Technical Reimbursement Component of Major Imaging Procedures, United States, 2011 and 2015

- 44. Professional Reimbursement Component of Major Imaging Procedures, United States, 2011 and 2015

- 45. Private Imaging Offices, United States, 2000–2012

- 46. Hospital Outpatient Departments (HOPD), United States, 2000–2012

- 47. Number of US Free-standing and Hospital Outpatient Imaging Centers United States, 2008–2013

- 48. Major Trends in Select Outpatient Imaging Center Chains (2015)

- 49. Clinical Laboratories Market: Revenues By Lab Type, United States, 2014–2018

- 50. Clinical Laboratories Market: Test Volumes by Specialty, United States, 2014

- 51. Clinical Laboratories Market, Market Share Analysis, US, 2014

- 1. The 12-step Market Insight Research Methodology Process

- 2. Lean Innovations and Management Principals to be Key

- 3. Rise of Smart Hospitals

- 4. Core Technology Architecture for Building a Smart Hospital—Enterprise Connectivity

- 5. Core Technology Architecture for Building a Smart Hospital—Devices and Sensors

- 6. Core Technology Architecture for Building a Smart Hospital—Healthcare IT

- 7. Mapping the Transformation of Care Provision

- 8. Assessing the Vendor Opportunity Landscape

- 9. US Hospitals—Snapshot of Current Status

- 10. What Keeps Hospital CEOs Awake at Night - Hospital Challenges

- 11. Key Hospital Objectives

- 12. Challenges Posed by the Affordable Care Act (ACA)

- 13. Hospital-owned Insurance Plans

- 14. Hospital Consolidation Overview

- 15. Role of ACOs

- 16. CMS Stipulations for Medicare ACOs

- 17. ACO Quality Measures—4 Key Domains

- 18. Role of ACOs in Chronic Disease Management

- 19. Changing Reimbursement Models

- 20. Types of Value-based Payments

- 21. Bundled Payments Landscape

- 22. Causes of Declining Hospital Inpatient Volumes (2006–2010)

- 23. Transition of Retail Clinics

- 24. Health Systems Partnerships With Retail Clinics

- 25. Ambulatory Care Model 5—Telemedicine in Rural Hospitals

- 26. Clinical Specialty Area 2—Cardiovascular Diseases (CVDs)

- 27. Clinical Specialty Area 3—Behavioral Health

- 28. Clinical Specialty Area 4—Long-term Care (LTC) Hospitals

- 29. Current HAI Prevention Measures Adopted by Hospitals

- 30. Solution for HAIs—CMS Partnership for Patients Program

- 31. Future Technology 1—Personalized Genetic Medicine

- 32. Future Technology 2—3D Printing

- 33. Future Technology 3—Nano Medicine

- 34. Benefits of Joint Ventures

- 35. Replacement of Joint Ventures—Rise of Hybrid Models

- 36. Hybrid Partnership Models—Examples

- 37. Clinical Laboratories in the United States - Lab Type

- 38. Emerging Trends in Key Specialty Areas

- 39. Hospitals and Independent Labs—Types of Partnerships

- 40. Acquisition of Outreach and Physician Office Labs

- 41. Acquisition of Specialty Labs

- 42. Point of Care Testing—The Next Big Thing

- 43. Evolution of the Healthcare Landscape: 2010–2020

- 44. From Episodic to Managed Care

- 45. A Healthcare Utopia—Vision for 2020 and Beyond

- 46. US Health Market Innovation Landscape - Technology Drives Innovation

- 47. Facilitating Continuum of Care Services

- 48. Role of Big Data

- 49. Creating Big Data Analytics Solutions

| No Index | No |

|---|---|

| Podcast | No |

| Table of Contents | | Research Methodology~ | Executive Summary~ | Influencers Impacting US Hospital Transformation~ || Evolution of New Models of Care Delivery~ || Competitor Influence~ ||| Pressure hospitals face~ ||| Moving beyond acute care setting~ ||| Re-structuring for consolidation~ || Lean Innovations and Management Principals to be Key~ ||| Infrastructure~ ||| Technology~ ||| Financial~ ||| Process Management~ ||| People~ || Rise of Smart Hospitals~ ||| Enterprise Connectivity~ ||| Devices and Sensors~ ||| Healthcare IT~ || Mapping the Transformation of Care Provision~ ||| Assessing the Vendor Opportunity Landscape~ | US Hospitals—Overview~ || Snapshot of Current Status~ || What Keeps Hospital CEOs Awake at Night~ || Key Hospital Objectives~ || Challenges Posed by the Affordable Care Act (ACA)~ || Financial Status—For-profit Hospitals~ || Financial Status—Not-for-profit Hospitals~ || Hospital-owned Insurance Plans~ || Financial Status—Rural Hospitals~ | Consolidations and Acquisitions among Hospitals~ || Healthcare Spending Landscape in the United States~ || Hospital Consolidation Overview~ || Hospital Services Expansion~ ||| Analysis of the 1,500 Hospital Acquisition Deals Between 2006 and 2014~ | Accountable Care Organizations (ACOs)~ || Role of ACOs~ || CMS Stipulations for Medicare ACOs~ || ACO Quality Measures—4 Key Domains~ ||| Patient / Caregiver Experience~ ||| Care Coordination / Patient Safety~ ||| Preventive Health~ ||| At-Risk Population~ || Role of ACOs in Chronic Disease Management~ || Accountable Care Organization—Infrastructure Landscape~ || Accountable Care Organization—Segment Landscape~ || Accountable Care Organization—Patient Coverage~ || Accountable Care Organization Model—Analysis~ || Changing Reimbursement Models~ || Types of Value-based Payments~ ||| Shared Savings~ ||| Shared Risk~ ||| Bundled Payments~ ||| Capitation~ || Bundled Payments Landscape~ | Impact of Medicare on Hospitals~ || Inpatient Landscape by Payor~ || Hospital Reimbursement Landscape~ || Medicare Advantage (MA) Plans~ | Hospital Inpatient Volume Snapshot~ || Inpatient Statistics Analysis~ || Hospital Inpatient Volume Trends~ ||| Causes of Declining Hospital Inpatient Volumes (2006–2010)~ ||| Causes of Declining Hospital Inpatient Volumes (2011–2015)~ || Financial Impact of Hospital Consolidations~ | Hospital Outpatient Volume Snapshot~ || Outpatient Statistics Analysis~ || Ambulatory Surgical Center Trends~ | Synergies of Tomorrow—Evolving Partnerships Between Hospitals and Ambulatory Care Providers~ || Ambulatory Care Provider Model 1—Retail Clinics~ || Future of Retail Clinics~ || Transition of Retail Clinics~ || Health Systems Partnerships With Retail Clinics~ || Ambulatory Care Provider Model 2—Urgent Care Clinics~ || Health Systems Partnerships With Urgent Care Clinics~ ||| Case Studies~ |||| Partnership Model~ |||| Hospital Set-Up Model~ || Ambulatory Care Provider Model 3—Bridge Clinics~ ||| Case Study: John Hopkins Heart Failure Clinic~ || Ambulatory Care Model 4—Virtualization of Primary Care~ || Ambulatory Care Model 5—Telemedicine in Rural Hospitals~ ||| Case Studies~ |||| Grande Ronde Hospital~ |||| VA Mayo Clinic Arizona~ |||| Lincoln Hospital~ | Current Therapeutic Service Lines Driving Hospital Revenues~ || Hospital Revenues by Key Specialties~ || Clinical Specialty Area 1—Orthopedics~ ||| Drivers~ ||| Constraints~ || Clinical Specialty Area 2—Cardiovascular Diseases (CVDs)~ || Clinical Specialty Area 2—Emergence of TAVR~ || Clinical Specialty Area 2—Emergence of TMVR~ || Clinical Specialty Area 3—Behavioral Health~ ||| American Adults (Ages 18 and Over)~ ||| American Children (Ages 13–18)~ || Clinical Specialty Area 4—Long-term Care (LTC) Hospitals~ || Hospital Acquired Infections—A Major Hospital Challenge~ || Solution for HAIs—CMS Partnership for Patients Program~ | Focus on Future Technologies Enabling Hospitals~ || Personalized Genetic Medicine~ || Case Studies~ ||| Mayo Clinic~ ||| Intermountain Precision Genomics~ ||| Cleveland Clinic~ ||| Children’s Hospital of Wisconsin~ || 3D Printing~ || Nano Medicine~ | Snapshot of Current and Future Trends in Medical Imaging~ || Summary of Medical Imaging Trends~ ||| Financial Challenges to Medical Imaging~ ||| Future Financial Challenges~ ||| Partnerships of the Future~ || Technical Reimbursements—Target of Medicare Cuts~ || Imaging Procedure Landscape~ || Imaging Centers—Facing a Tough Economic Environment~ || Joint Ventures—An Attractive New Model of Collaboration~ || Benefits of Joint Ventures~ ||| Health System Benefits ~ ||| Mutual Benefits ~ ||| Imaging Center Benefits~ || Replacement of Joint Ventures—Rise of Hybrid Models~ || Hybrid Partnership Models—Examples~ | Snapshot of Current and Future Trends in Clinical Laboratories~ || Summary of Clinical Laboratory Trends~ ||| Financial Challenges to Diagnostic Labs~ ||| Future Models of Partnership~ ||| Point of Care (PoC) Testing~ || Clinical Laboratories in the United States—Snapshot~ || Clinical Laboratories—Key Specialty Areas of Focus~ || Decentralization of Clinical Laboratory Testing~ || Hospitals and Independent Labs—Types of Partnerships~ || Independent Clinical Labs—Consolidation Trends~ || Point of Care Testing—The Next Big Thing~ | An Ideal Vision of the Future of Care Provision in the United States~ || Evolution of the Healthcare Landscape: 2010–2020~ || Key Healthcare Trends: 2016–2020~ || From Episodic to Managed Care~ || A Healthcare Utopia—Vision for 2020 and Beyond~ || Healthcare Innovation will Drive New Market Opportunities~ || Facilitating Continuum of Care Services~ || Role of Big Data~ || Creating Big Data Analytics Solutions~ ||| Imaging files~ ||| Genomic data~ ||| Clinician notes~ ||| Others ~ | Legal Disclaimer~ | Appendix~ || Definitions of Key Terms~ | The Frost & Sullivan Story~ || Value Proposition: Future of Your Company & Career~ || Global Perspective~ || Industry Convergence~ || 360º Research Perspective~ || Implementation Excellence~ || Our Blue Ocean Strategy~ |

| List of Charts and Figures | 1. Financial Status—For-profit Hospitals~ 2. Median Annual Revenue Growth, United States, 2013–2014 ~ 3. Median Annual Expenditure Growth, United States, 2012–2014~ 4. Rural Hospital Closures, United States, 2010–Q32015 ~ 5. Healthcare Spending, United States, 2013 ~ 6. Healthcare Spending by Payer, United States, 2013~ 7. Hospital Acquisition Deals, United States, 2006–2010~ 8. Hospital Acquisition Deals, United States, 2010–2014 ~ 9. Growth in ACOs, United States, 2011–Q12015~ 10. Growth in ACO Contracts, United States, 2011–2014~ 11. Breakup of ACOs by Ownership, United States, 2015~ 12. ACO Population Coverage, United States, 2011–2020~ 13. Reduction in Number of Pioneer ACOs, United States, 2012–2014~ 14. Patients Treated in Hospitals by Payer, United States, 2013~ 15. Medicare FFS Payments for Hospital Inpatient & Outpatient Services*, United States, 2005–2013~ 16. Medicare Spending Trends~ 17. Medicare Advantage Enrollees, United States, 2009–2015~ 18. Distribution of Enrollees, United States, 2015~ 19. Inpatient Admissions/1,000 Population, United States, 2005–2013~ 20. Inpatient Surgeries Performed, United States, 2005–2013~ 21. Inpatient Days/1,000 Population, United States, 2005–2013~ 22. Total Inpatient Days, United States, 2005–2013~ 23. Markup of Hospital Charges Above Costs For Medicare Services, United States, 2005–2012~ 24. Top 50 Hospitals in Terms of Markups~ 25. Outpatient Visits/1,000 Population, United States, 2005–2013~ 26. Total Outpatient Visits, United States, 2005–2013~ 27. Total Outpatient Surgeries, United States, 2005–2013~ 28. ASC Growth Trends, United States, 2008–2014~ 29. Number of Retail Clinics, United States, 2009–2021~ 30. Patients Visiting Retail Clinics, United States, 2013–2021~ 31. Retail Clinic Revenues, United States, 2013–2021~ 32. Urgent Care Clinic Ownership, United States, 2015~ 33. Virtual Doctor Consultations*, United States, 2015–2020~ 34. Hospital Revenues by Key Specialties ~ 35. Increasing Annual CMS Spending on Hip and Knee Bundles, United States, 2016–2020~ 36. Incidence of Aortic Stenosis, United States, 2015–2025~ 37. Incidence of Severe Mitral Regurgitation, United States, 2015–2025 ~ 38. Clinical Specialty Area 3—Behavioural Health~ 39. Rising Costs of LTC~ 40. Percentage Split of Medicaid Spending on LTC, United States, 2005–2013 ~ 41. Clinical Specialty Area 4 - LTC Facilities~ 42. Clinical Specialty Area 4 - Medicare Spending~ 43. Technical Reimbursement Component of Major Imaging Procedures, United States, 2011 and 2015 ~ 44. Professional Reimbursement Component of Major Imaging Procedures, United States, 2011 and 2015~ 45. Private Imaging Offices, United States, 2000–2012~ 46. Hospital Outpatient Departments (HOPD), United States, 2000–2012~ 47. Number of US Free-standing and Hospital Outpatient Imaging Centers United States, 2008–2013 ~ 48. Major Trends in Select Outpatient Imaging Center Chains (2015) ~ 49. Clinical Laboratories Market: Revenues By Lab Type, United States, 2014–2018 ~ 50. Clinical Laboratories Market: Test Volumes by Specialty, United States, 2014 ~ 51. Clinical Laboratories Market, Market Share Analysis, US, 2014~| 1. The 12-step Market Insight Research Methodology Process~ 2. Lean Innovations and Management Principals to be Key~ 3. Rise of Smart Hospitals~ 4. Core Technology Architecture for Building a Smart Hospital—Enterprise Connectivity~ 5. Core Technology Architecture for Building a Smart Hospital—Devices and Sensors~ 6. Core Technology Architecture for Building a Smart Hospital—Healthcare IT~ 7. Mapping the Transformation of Care Provision~ 8. Assessing the Vendor Opportunity Landscape~ 9. US Hospitals—Snapshot of Current Status~ 10. What Keeps Hospital CEOs Awake at Night - Hospital Challenges~ 11. Key Hospital Objectives~ 12. Challenges Posed by the Affordable Care Act (ACA)~ 13. Hospital-owned Insurance Plans~ 14. Hospital Consolidation Overview~ 15. Role of ACOs~ 16. CMS Stipulations for Medicare ACOs~ 17. ACO Quality Measures—4 Key Domains~ 18. Role of ACOs in Chronic Disease Management~ 19. Changing Reimbursement Models~ 20. Types of Value-based Payments~ 21. Bundled Payments Landscape~ 22. Causes of Declining Hospital Inpatient Volumes (2006–2010)~ 23. Transition of Retail Clinics~ 24. Health Systems Partnerships With Retail Clinics~ 25. Ambulatory Care Model 5—Telemedicine in Rural Hospitals~ 26. Clinical Specialty Area 2—Cardiovascular Diseases (CVDs)~ 27. Clinical Specialty Area 3—Behavioral Health~ 28. Clinical Specialty Area 4—Long-term Care (LTC) Hospitals~ 29. Current HAI Prevention Measures Adopted by Hospitals~ 30. Solution for HAIs—CMS Partnership for Patients Program~ 31. Future Technology 1—Personalized Genetic Medicine~ 32. Future Technology 2—3D Printing~ 33. Future Technology 3—Nano Medicine~ 34. Benefits of Joint Ventures~ 35. Replacement of Joint Ventures—Rise of Hybrid Models~ 36. Hybrid Partnership Models—Examples~ 37. Clinical Laboratories in the United States - Lab Type~ 38. Emerging Trends in Key Specialty Areas~ 39. Hospitals and Independent Labs—Types of Partnerships~ 40. Acquisition of Outreach and Physician Office Labs~ 41. Acquisition of Specialty Labs~ 42. Point of Care Testing—The Next Big Thing~ 43. Evolution of the Healthcare Landscape: 2010–2020~ 44. From Episodic to Managed Care~ 45. A Healthcare Utopia—Vision for 2020 and Beyond~ 46. US Health Market Innovation Landscape - Technology Drives Innovation~ 47. Facilitating Continuum of Care Services~ 48. Role of Big Data~ 49. Creating Big Data Analytics Solutions~ |

| Author | Tanvir Jaikishen |

| WIP Number | K01B-01-00-00-00 |

| Is Prebook | No |