USD

USD GBP

GBP CNY

CNY EUR

EUR INR

INR JPY

JPY MYR

MYR ZAR

ZAR KRW

KRW THB

THBHow Sustainability Trends are Affecting the Global Plastics Industry, 2017–2026

How Sustainability Trends are Affecting the Global Plastics Industry, 2017–2026

Manufacturers are Under Pressure to Create a Circular Economy for All Plastics and Use Alternative Materials Whenever Possible

30-May-2019

Global

$4,950.00

Special Price $3,712.50 save 25 %

Description

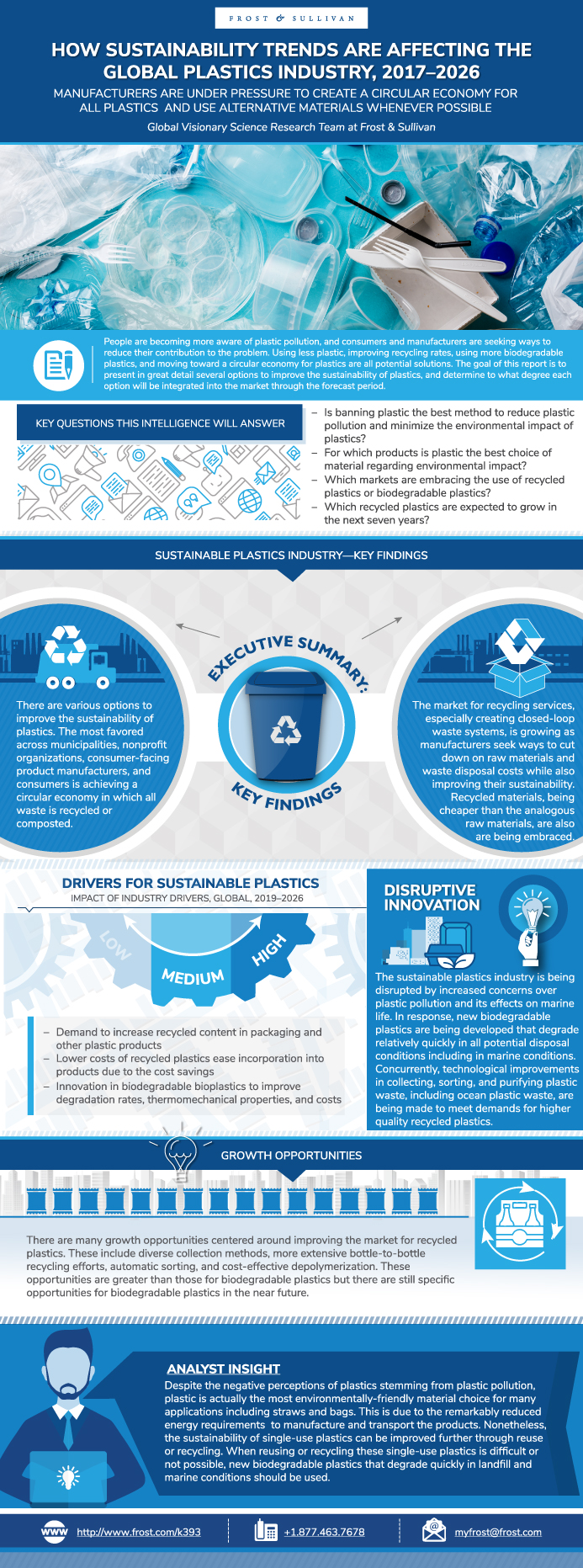

People are becoming more aware of plastic pollution, and consumers and manufacturers are seeking ways to reduce their contribution to the problem. Using less plastic, improving recycling rates, using more biodegradable plastics, and moving toward a circular economy for plastics are all potential solutions. The goal of this report is to present in great detail several options to improve the sustainability of plastics, and determine to what degree each option will be integrated into the market through the forecast period. For example, alternatives to plastic are discussed and segmented into specific applications. The environmental impact of paper or metal straws, cloth bags, paper cups, and other plastic alternatives are discussed, and the most environmentally friendly options are highlighted for each application.

In-depth primary and secondary research is the foundation of this report. Companies all along the supply chain were consulted to gain a thorough overview of the sustainable plastics market. This research also builds off of years of research done at Frost & Sullivan in terms of understanding how the thermoplastics industry is being affected by growing concerns over the environmental impact of plastics.

Market information and forecasts for the thermoplastics, recycled thermoplastics, and bioplastics markets are given for 2017 to 2026. These markets are broken down by region, type of plastic, and industry. The market drivers and restraints for each forecast are discussed to provide additional context. Key manufacturers in each of these markets are also discussed. The prospects of the recycled plastics and bioplastics are dependent on the type of plastic, so more information is provided about the differences. HDPE and PET, for example, are large parts of the recycled plastics market, while the recycled polystyrene market is much smaller. Reasons for this are discussed, and innovations that can improve recycling rates of polystyrene are included.

The effects of regulations and recent regulatory enforcement are also discussed. Countries have different policies on plastics. Plastic bags have been banned in many locations, and bans on other single-use plastics are being endorsed and ratified. Additional governmental policies, such as the recent changes in China’s policies on scrap plastic imports, are also examined. These regulations affect the growth of the plastics market in general as well as how quickly plastics become more environmentally friendly.

Ten growth opportunities for plastic manufacturers are also provided. These incorporate the expected forecasts and how manufacturers can best leverage the changes in the plastics market. The opportunities include the development or increased use of new technologies, new collection methods, increasing the use of specific sources of plastic waste, and certain business strategies. By implementing these strategies, manufacturers and processors of plastic waste can capture more of the sustainable plastics market as it quickly grows in the next decade.

RESEARCH: INFOGRAPHIC

This infographic presents a brief overview of the research, and highlights the key topics discussed in it.Click image to view it in full size

Table of Contents

Strategic Imperative

Study Scope

Sustainable Plastics Industry—Key Findings

Sustainable Plastics Industry—Key Findings (continued)

Sustainability Goals—Minimizing Environmental Impact

Methods to Minimize Environmental Impact—Alternative Materials

Methods to Minimize Environmental Impact—Biodegradable Plastics

Methods to Minimize Environmental Impact— Biodegradable Plastics (continued)

Methods to Minimize Environmental Impact—Recycling

Methods to Minimize Environmental Impact—Recycling (continued)

Effect of Regulations on Environmental Impact

Effect of Regulations on Environmental Impact (continued)

Sustainable Plastics Supply Chain—End-Use Consumers

Sustainable Plastics Supply Chain—Manufacturers

Sustainable Plastics Supply Chain—OEMs and Consumer-Facing Manufacturers

Growth Opportunities in the Sustainable Plastics Industry

Growth Opportunities in the Sustainable Plastics Industry (continued)

Growth Opportunities in the Sustainable Plastics Industry (continued)

Growth Opportunities in the Sustainable Plastics Industry (continued)

Sustainable Plastics

Sustainable Plastics—Sources for Manufacturing

Sustainable Plastics—Sustainable Designs

Recycling

Recycled Plastics—Typical Uses

Recycled Plastics—Commodity and High-Performance Polymers

Biodegradation

Biodegradation (continued)

Bioplastics—Typical Uses

6 Biodegradable Bioplastics

Types of Biodegradable Plastics

Types of Biodegradable Plastics (continued)

Types of Biodegradable Plastics (continued)

15 Nonbiodegradable Bioplastics

Types of Nonbiodegradable Bioplastics

Drivers for Sustainable Plastics

Drivers for Sustainable Plastics Explained

Restraints for Sustainable Plastics

Restraints for Sustainable Plastics Explained

Thermoplastics Overview

Drivers for Thermoplastics

Drivers for Thermoplastics Explained

Restraints for Thermoplastics

Restraints for Thermoplastics Explained

Thermoplastics Industry—Volume Share by Polymer

Thermoplastics Industry—Revenue Share by Polymer

Thermoplastics Industry—Revenue Forecast by Polymer

Thermoplastics Industry—Price Forecast by Polymer

Thermoplastics Industry—Revenue Share Forecast by End-Use Industry

Thermoplastics Industry—Revenue Forecast by End-Use Industry

Sustainable Plastics Industry—Nonprofit Organizations and Government Agencies

Sustainable Plastics Supply Chain—Waste Processors

Sustainable Plastics Supply Chain—Resin Manufacturers

Sustainable Plastics Supply Chain—OEMs

Sustainable Plastics Supply Chain—Consumer-facing Manufacturers

Sustainable Plastics Supply Chain—End-Use Consumers

Sustainable Plastics Supply Chain—End-Use Consumers (continued)

Methods to Reduce Plastic Use

Alternatives to Microplastics in Cosmetics

Alternatives to Plastic for Carry-Out Bags

Alternatives to Plastic Packaging

Alternatives to Plastic Packaging (continued)

Alternatives to Plastic Cutlery and Dishware

Alternatives to Plastic Straws

Sustainable Designs

Summary of Plastic Reduction

Summary of Plastic Reduction (continued)

Choice of Sustainable Plastic

Recycled Plastics Overview and Trends

Recycled Plastics Overview and Trends (continued)

Drivers for Recycled Plastics

Drivers for Recycled Plastics Explained

Restraints for Recycled Plastics

Restraints for Recycled Plastics Explained

Recycled Thermoplastics Industry—Revenue Forecast

Recycled Thermoplastics Industry—Volume Forecast

Recycled Thermoplastics Industry—Volume Shipment Share Forecast by Polymer

Recycled Thermoplastics Industry—Revenue by Region

Recycled Thermoplastics Industry—Price Forecast

Current Industry Information—Price by Resin

Recycled Plastics Industry Information—Price Analysis

Thermoplastics Industry—Recycled Plastics by Resin

Thermoplastic Properties

HDPE Industry—Applications

Recycled HDPE Industry Overview

Recycled HDPE Industry—Revenue Forecast

Recycled HDPE Industry—rHDPE Manufacturers

LDPE Industry—Applications

Recycled LDPE Industry—Overview

LDPE Industry—Revenue Forecast

Recycled LDPE Industry—rLDPE Manufacturers

PET Industry—Applications

Recycled PET Industry—Overview

Recycled PET Industry—Revenue Forecast

Recycled PET Industry—rPET Manufacturers

Recycled PET Industry—rPET Manufacturers (continued)

PP Industry—Applications

Recycled PP Industry—Overview

Recycled PP Industry—Revenue Forecast

Recycled PP Industry—rPP Manufacturers

PVC Industry—Applications

Recycled PVC Industry—Overview

Recycled PVC Industry—Revenue Forecast

Recycled PVC Industry—rPVC Manufacturers

PA Industry—Applications

Recycled PA Industry—Overview

Recycled PA Industry—Revenue Forecast

Recycled PA Industry—rPA Manufacturers

PS Industry—Applications

Recycled PS Industry—Overview

Recycled PS Industry—rPS Manufacturers

ABS Industry—Applications

Recycled ABS Industry—Overview

Recycled ABS Industry—rABS Manufacturers

PC Industry—Applications

Recycled PC Industry—Overview

Recycled PC Industry—rPC Manufacturers

Acrylic Industry—Applications

Recycled Acrylic Industry—Overview

Recycled Acrylic Industry—Manufacturers

TPE Industry—Applications

TPE Industry—Resin Comparison

TPE Industry—Resin Comparison (continued)

TPE—Sustainability

High-Performance Resin Industry

Recycled Thermoplastic Industry—Top Recycling Companies

Recycled Thermoplastic Industry—Top Product Specifications

Regional Recycling Variations—North America

Regional Recycling Variations—North American Processors

Regional Recycling Variations—Europe

Regional Recycling Variations—European Industry Leaders

Regional Recycling Variations—Asia

Regional Recycling Variations—Asian Industry Leaders

Regional Variations—ROW

Regional Variations—ROW (continued)

Choice of Sustainable Plastic

Bioplastics Industry—Types of Bioplastics

Biodegradable Plastics Overview

Drivers for Bioplastics

Drivers for Bioplastics Explained

Restraints for Bioplastics

Restraints for Bioplastics Explained

Bioplastics Industry—Revenue Forecast

Bioplastics Industry—Volume Forecast

Bioplastics Industry—Revenue Forecast by Resin Type

Bioplastics Industry—Volume Forecast by Resin Type

Bioplastics Industry—Revenue Forecast by Region

Bioplastics Industry—Pricing Trends

Global Pricing Trends for Bioplastics

Bioplastics Industry—Volume Share by Application

Bioplastics Industry—PLA

Bioplastics Industry—PLA Revenue Forecast

Bioplastics Industry—PHA

Bioplastics Industry—PHA Revenue Forecast

Bioplastics Industry Challenges

Bioplastics Industry—Challenges Explained

Bioplastics Industry—Challenges Explained (continued)

Bioplastics Industry—Key Challenges and Barrier-Breaking Implications

Bioplastics Industry—Competitive Factors

Regulatory Overview

Bans on Single-Use Plastics

Bans on Single-Use Plastics (continued)

EU Strategy on Plastics

Regulations on Recycling

Regulations on Bioplastics

Regulations on Biodegradable Plastics

US Regulations on Sustainable Plastics

US Regulations on Sustainable Plastics (continued)

Regulatory Enforcement

Industry Trends

Industry Outlook

Growth Opportunity 1—Automated Sorting

Growth Opportunity 2—Bottle-to-Bottle Recycling

Growth Opportunity 3—Recycling Reinforced Plastics

Growth Opportunity 4—Recycling High-Value Plastics

Growth Opportunity 5—Cost-Effective Depolymerization

Growth Opportunity 6—Marine and Landfill Biodegradation for Single-Use Plastics

Growth Opportunity 7—Improve Worldwide Recycling Infrastructure

Growth Opportunity 8—Vertical Integration

Growth Opportunity 9—Closed-Loop Recycling

Growth Opportunity 10—Ocean Plastic Collection

Other Growth Opportunities in the Sustainable Plastics Industry

Strategic imperatives for Growth of the Sustainable Plastics Industry

The Last Word—The Future of Sustainable Plastic

The Last Word—3 Big Predictions

Legal Disclaimer

Abbreviations

Abbreviations (continued)

Links to Selected Secondary Sources

Links to Selected Secondary Sources (continued)

Links to Selected Secondary Sources (continued)

Links to Selected Secondary Sources (continued)

List of Exhibits

List of Exhibits (continued)

List of Exhibits (continued)

List of Exhibits (continued)

The Frost & Sullivan Story

Value Proposition: Future of Your Company & Career

Global Perspective

Industry Convergence

360º Research Perspective

Implementation Excellence

Our Blue Ocean Strategy

Popular Topics

| No Index | No |

|---|---|

| Podcast | No |

| Author | Ranulfo Allen |

| Industries | Chemicals and Materials |

| WIP Number | K393-01-00-00-00 |

| Is Prebook | No |

| GPS Codes | 9100-A2,9869-A2,9938-A2,9595,9870 |