Indian Calcium Carbonate (CaCO3) Market, Forecast to 2021

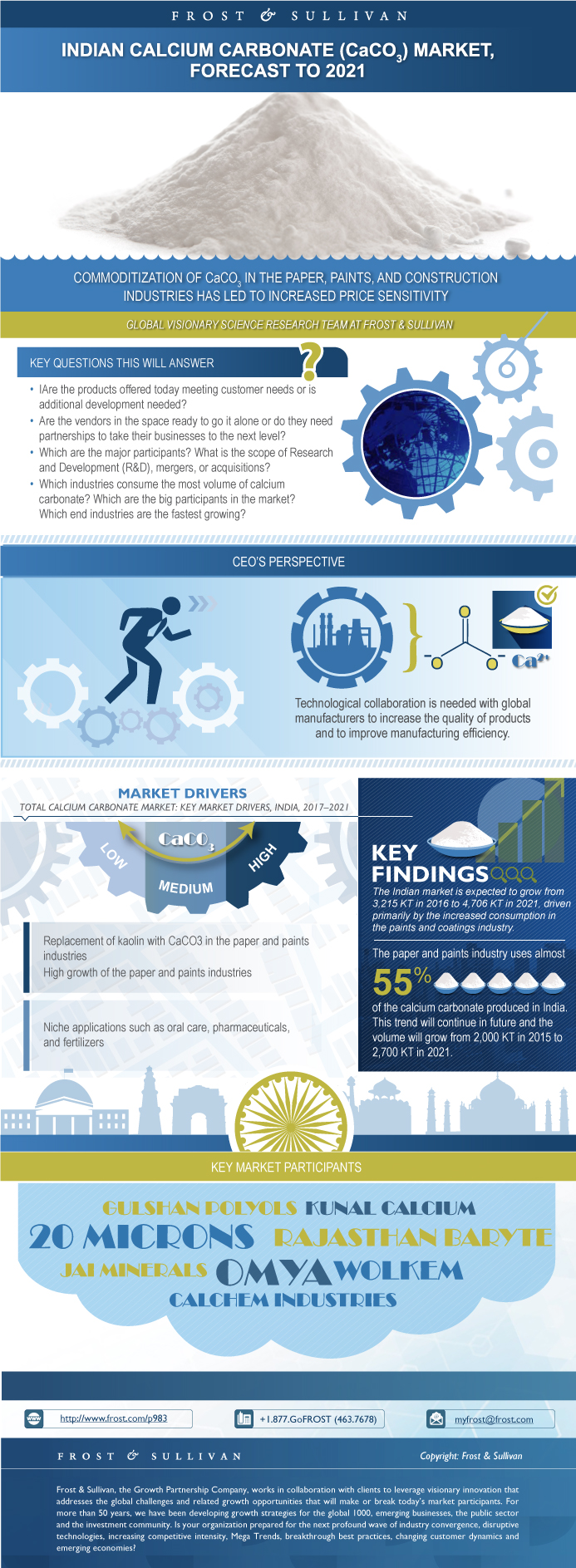

Commoditization of CaCO3 in the Paper, Paints, and Construction Industries has led to Increased Price Sensitivity

27-Dec-2017

South Asia, Middle East & North Africa

Market Research

P983-01-00-00-00

CM01517-SA-MR_21370

$4,950.00

Special Price $3,712.50 save 25 %

Calcium carbonate has historically been one of the preferred fillers for the paper industry. In recent years, it has also become a preferred filler for the paint industry, heavily substituting kaolin in this application. While the primary reason has been the unavailability of high-quality kaolin, customers are also shifting due to the better opacity, gloss, and scrub resistance provided by calcium carbonate. While paint and paper are likely to remain the main application focus for calcium carbonate, relatively higher growth in segments such as Poly Vinyl Chloride (PVC) and masterbatches offer significant potential for a supplier to target, primarily due to the large expansion plans of companies such as Plastiblends and Finolex in India. Additionally, there is significant import substitution potential for steric coated grades of Ground Calcium Carbonate (GCC) and Precipitated Calcium Carbonate (PCC) in masterbatches and PVC applications.

The key challenge suppliers face today is delivering high product performance in what has become a highly commoditized market. Inclusion of niche grades (such as steric coated for masterbatches and PVC) and application development along with the end user has to be the focus for suppliers looking to make premium offerings and improving their margins. However, this can only be in addition to the high-volume sales of commodity grades, as the potential to make premium calcium carbonate offerings in India remains low.

The demand for PCC is limited by its niche application segments and its price. Even though PCC finds niche usage in applications such as pharmaceuticals and oral care, there are alternate fillers also which are also fulfilling the needs of the respective industry. As a result, GCC accounts for 85% of the calcium carbonate consumed today, while PCC is only 15% of the nearly 3 million MT market size. This market is serviced by 4 large-scale calcium carbonate producers that account for around 30% of the market and an additional 20%–22% of the demand is met by imports. The remainder of the market is fragmented and is catered to by medium, small-scale, and unorganized producers.

Research Scope:

This study covers the Indian market for both types of calcium carbonate in India and provides strategic insights with respect to growth opportunities. The study further captures the value chain of the Indian Calcium Carbonate market and looks to understand the projected market value by type and application. Additionally, it provides an overview of the key trends, drivers and restraints, and critical success factors for calcium carbonate manufacturers supplying to the Indian market. Overall, this study aims to assess the potential of calcium carbonate in India and understand how it is expected to evolve in the near future.

Key Findings

Market Engineering Measurements

CEO’s Perspective

Market Definitions

Product Definitions

Market Trends

Key Questions This Study Will Answer

Market Segmentation

Market Segmentation—GCC

Market Segmentation—PCC

Market Distribution Channels

Market Drivers

Drivers Explained

Market Restraints

Restraints Explained

Market Engineering Measurements

Forecast Assumptions

Volume Forecast

GCC Percent Volume Forecast by Segment

PCC Percent Volume Forecast by Segment

Key Trends Driving the GCC and PCC Markets

Market Share—Total Calcium Carbonate Market

Market Share—GCC Market

Market Share—PCC Market

Market Share Analysis—GCC Market

Market Share Analysis—PCC Market

Competitive Environment

Top Competitors

Competitive Factors and Assessment

Growth Opportunity: Infrastructure Growth

Growth Opportunity: Growth in Major End-Use Industries

Growth Opportunity: Import Substitution

Growth Opportunity: Kaolin Substitution

Growth Opportunity: India’s Focus on Becoming a Manufacturing Hub

Strategic Imperatives for CaCO3 Manufacturers

Market Engineering Measurements

Volume Forecast

Key Upcoming Plants in the Paper Industry

Market Engineering Measurements

Volume Forecast

Key Upcoming Plants in the Paints Industry

Market Engineering Measurements

Volume Forecast

Key Upcoming Plants in the Plastics Industry

Market Engineering Measurements

Volume Forecast

The Last Word—3 Big Predictions

Legal Disclaimer

Market Engineering Methodology

Abbreviations and Acronyms Used

Speak directly with our analytics experts for tailored recommendations.

Recent related CASE & Construction Chemicals research

24 Jul 2026 | Global | Market Research

Regulatory Trends Impacting the Chemical Industry, 2026

This study analyzes the impact of evolving regulatory frameworks across the chemical industry, focusing on both product-level and end-industry regulations. The scope spans key product segments including coatings, adhesives and sealants, polymers and composites, fuels and lubricants, and process chem...

22 Apr 2026 | Global | Technology Research

Data-Driven Materials Informatics for Accelerated Polymer, Coatings, and Catalyst Innovation

Data-driven materials informatics is transforming the discovery and development of advanced materials, enabling faster innovation across polymers, coatings, and catalytic systems. By integrating experimental data, computational simulations, and AI and ML models, these platforms enable predictive des...

10 Mar 2026 | Global | Strategic Imperatives

Top 10 Strategic Imperatives in the Construction Materials Industry, 2026

This report examines the key strategic transformations shaping growth in the construction materials industry throughout 2026 and beyond. It analyzes the impacts of geopolitical instability on supply chains, resulting in cost volatility, increased localization of production, and diversification of ra...

22 Jan 2026 | Global | Technology Research

Nanoporous Catalysts for Optimized Efficiency in Chemical Processing and Industrial Reactions

Global industries are entering a new phase of efficiency-driven transformation, where material innovation underpins competitive advantage and sustainability compliance. Within this landscape, nanoporous catalysts have emerged as a pivotal enabler—driving faster reaction kinetics, superior selectiv...

24 Dec 2025 | Global | Market Research

Digital Transformation in the Construction Materials Industry, Global, 2025

Digital transformation in the building materials industry involves integrating digital technologies and data-driven processes across every facet of a company’s operations, including supply chain management, design, production, sourcing, and customer interactions. The goals are to increase producti...

Purchase includes:

- Report download

- Growth Dialog™ with our experts

Growth Dialog™

A tailored session with you where we identify the:- Strategic Imperatives

- Growth Opportunities

- Best Practices

- Companies to Action

Impacting your company's future growth potential.

| Deliverable Type | Market Research |

|---|---|

| No Index | No |

| Podcast | No |

| Author | Govind Ramakrishnan |

| Industries | Chemicals and Materials |

| WIP Number | P983-01-00-00-00 |

| Is Prebook | No |