Strategic Analysis of the Electric Vehicle Charging Infrastructure in China, 2018–2025

With the Increase in the Number of Electric Vehicles, Public Charging Points in Operation are Likely to Reach 4 Million Units by 2025

02-Aug-2019

Asia Pacific

Market Research

PA68-01-00-00-00

AU01875-AP-MR_23403

$3,000.00

Special Price $2,250.00 save 25 %

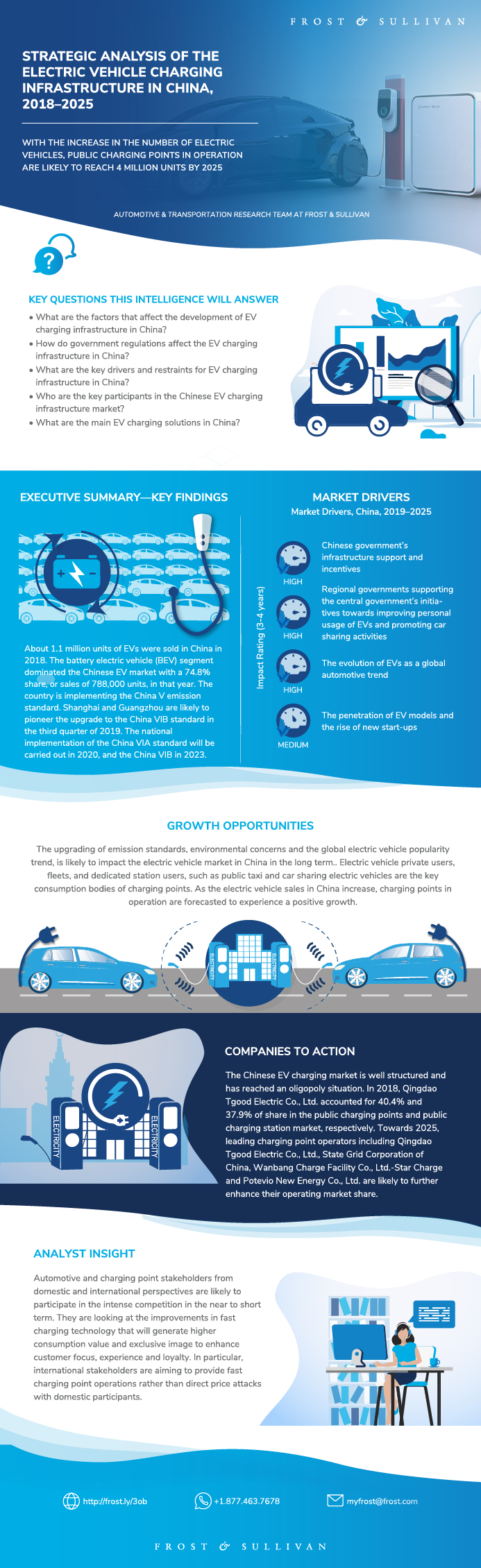

About 1.05 million units of electric vehicles (EVs) were sold in China in 2018. Battery electric vehicle (BEV) segment dominated the Chinese EV market with a 74.8% share, or sales of 788,000 units, in the year. The country is implementing the China V emission standard. Shanghai and Guangzhou are likely to pioneer the upgrade to the China VIB standard in the third quarter of 2019. The national implementation of the China VIA standard will be carried out in 2020 and the China VIB in 2023.

In 2018, there were a total of 808,300 charging points (piles) in operation. Overall, the total number of operating public charging points reached 331,300 units. The Chinese government encourages automotive original equipment manufacturers (OEMs) to provide the installation of private charging points. These charging points are privately owned by individual EV users and are installed in their own residential parking spaces.

The Chinese central government has revised the GB/T 20234 in 2015. Domestic and international stakeholders are encouraged to align with Guobiao (GB) standard plugs and connectors, including alternating current (AC) and direct current (DC) charging couplers. The government has framed various regulations and to accelerate the construction of charging points and facilitating interoperability between them. It also provides charging infrastructure incentives to regional governments, when they achieve large-scale implementation of EVs.

The public charging infrastructure is well established in Beijing, Shanghai and Guangdong, with them having 144,200 charging points combined, accounting for 43.5% of the market share in 2018. Qingdao Tgood Electric Co., Ltd., State Grid Corporation of China, and Wanbang Charge Facility Co., Ltd.-Star Charge are the key charging point operators who together cover 77.5% of the total public charging points in the country. With charging infrastructure being an emerging market in China, it is competitive and sees the presence of many stakeholders from different backgrounds, such as China Petroleum & Chemical Corporation (Sinopec) from the oil & gas industry, and DiDi Chuxing Technology Co., Ltd. from the shared mobility services space.

The Chinese central government plans to develop more than 800 fast charging stations in the country by 2020, mainly in the eastern region. The focus will be on the intercity areas, especially the expressway service areas, key economic zones and event venues, such as the Pearl River Delta, the Yangtze River Delta, and the Yanqing Winter Olympic Electric Vehicle Demonstration Zone (Beijing). State Grid Corporation of China is mainly concentrated on the expressways. Other notable stakeholders in developing the fast charging infrastructure in China include Tesla Inc., BP PLC, Guangzhou Xiaopeng Motors Technology Co., Ltd. and Wanbang Charge Facility Co., Ltd.-Star Charge. The goal of the maximum super-fast charge system is 1000V in the near future.

Research Scope

The aim of this study is to research and analyze the EV charging infrastructure market in China. The market has 3 distinct segments, namely public operations (for example, at expressways, commercial areas, and neighborhood areas); dedicated operations owned by fleet companies (for example, public taxis); and private charging infrastructure that is installed and owned by EV buyers at their homes and is available for their personal use. This study presents the current scenario in the charging market in China and provides a forecast for charging points up to 2025.

Key Features

Research Objectives:

- To provide a strategic perspective of the charging market for passenger vehicles in China, including market drivers, market restraints, and SWOT analysis.

- To give an overview of government policies that affect electrification and charging solutions.

- To analyze the charging market value chain, including key market participants, key projects, and investments.

- To estimate the size and development potential of the charging points in China towards 2025.

- To present an actionable set of recommendations for stakeholders to grow in the charging market in China.

Key Issues Addressed

- What are the factors that affect the development of the EV charging infrastructure in China?

- How do the government regulations affect the EV charging infrastructure in China?

- What are the key drivers and restraints for EV charging infrastructure in China?

- Who are the key market participants in the Chinese EV charging market?

- What are the main EV charging solutions in China?

Author: Chan Ming Lih

Executive Summary—Key Findings

Executive Summary—Market Engineering Measurements

Executive Summary—Passenger Vehicle Market Snapshot

Executive Summary—EV Charging Infrastructure Snapshot

Executive Summary—EV Charging Infrastructure Business Models

Executive Summary—SWOT Analysis

Research Scope

Research Aims and Objectives

Key Questions this Study will Answer

Research Methodology

Market Drivers

Drivers Explained

Drivers Explained (continued)

Market Restraints

Restraints Explained

Restraints Explained (continued)

Government Regulations

Government Regulations—Charging Infrastructure Incentive

Market Overview—Passenger Vehicle Powertrain Snapshot in 2018

Market Overview—EV Market Snapshot in 2018

Market Overview—Emission Standard

EV Charging Infrastructure—Main Charging Solutions in China

EV Charging Infrastructure—Standards of Charging Equipment

EV Charging Infrastructure—Value Chain Snapshot

EV Charging Infrastructure—Key Participants in the Value Chain

EV Charging Infrastructure—Business Models

Case Study—Private-Owned EV Charging Infrastructure with Wanbang NE

Fast Charging—Key Development Plan of the Chinese Government

Fast Charging—Key Regional Development Plans

Fast Charging—Key Developments by Key Stakeholders

Forecast and Trends—Market Engineering Measurements

Forecast and Trends—Public Charging Points Scenario Analysis

Forecast and Trends—Forecast Scenario Assumptions to 2025

Competitive Analysis—EV Charging Infrastructure Snapshot 2018

Competitive Analysis—EV Charging Infrastructure Breakdown by Region

Competitive Analysis—EV Charging Infrastructure Market Share

Competitive Analysis—Future EV Charging Infrastructure Market Developments

Case Study—Average Charging Price by Leading Market Participants

Charging Service Provider—State Grid Corporation of China

Charging Service Provider—Qingdao Tgood Electric Co., Ltd.

Charging Service Provider—Potevio New Energy Co., Ltd.

Charging Service Provider—BYD Co., Ltd.

Charging Service Provider—Individual EV Buyers

Case Study—Zhongchuang Sanyou, Integrates City-Level Charging Points

Case Study—DiDi (Xiaoju Charging), Operates Charging Points

Case Study—SAIC (Anyo Charging), Engaged in Charging Operations

Growth Opportunity—EV Charging Infrastructure for Passenger Vehicles in China

Strategic Imperatives for Success and Growth

Key Conclusions and Future Outlook

The Last Word—3 Big Predictions

Legal Disclaimer

Abbreviations and Acronyms Used

List of Exhibits

List of Exhibits (continued)

List of Exhibits (continued)

List of Exhibits (continued)

List of Exhibits (continued)

The Frost & Sullivan Story

Value Proposition—Future of Your Company & Career

Global Perspective

Industry Convergence

360º Research Perspective

Implementation Excellence

Our Blue Ocean Strategy

Speak directly with our analytics experts for tailored recommendations.

Recent related Aftermarket research

23 Jul 2026 | Global | Market Outlook

Growth Opportunities in the Automotive Aftermarket, Global, 2026

The global automotive aftermarket for light vehicles (≤6T GVWR) continues to demonstrate resilience despite moderating momentum in new vehicle sales. With a base year of 2025, this study evaluates market trends through 2030, providing a global perspective with region-specific insights for North Am...

20 Jul 2026 | North America | Market Research

Passenger Car & Light Truck Driveline Components Aftermarket, North America, 2026–2032

This Frost & Sullivan analysis of the North American passenger car and light truck driveline components aftermarket examines the volume and value of the industry for driveline components, specifically driveshafts and U-joints, in North America. The report discusses replacement rates and average manu...

29 Jun 2026 | Europe | Market Research

Passenger Vehicle Replacement Lead-Acid Battery Aftermarket, Europe, 2026–2032

The European lead-acid battery market for cars holds strong importance in the transport sector. These batteries remain the go-to choice for starting, lighting, and ignition (often called SLI) in vehicles with internal combustion engines, mild hybrids, and micro-hybrids that feature start-stop system...

29 Apr 2026 | South Asia, Middle East & North Africa | Customer Research

Voice of Consumer: Willingness and Desirability Toward Multi-Channel eCommerce Models, India, 2024

This Frost & Sullivan Voice of Consumer report analyzes how Indian passenger vehicle owners engage with multi-channel eCommerce for automotive spare parts across both online and offline touchpoints. The study profiles buyers by mapping their spending levels and category preferences, and examining th...

21 Apr 2026 | Global | Market Outlook

Growth Opportunities for the 2026 Medium- and Heavy-Duty Commercial Vehicle Aftermarket

The global medium- and heavy-duty commercial vehicle aftermarket is undergoing a structural transition. In 2025, global sales of new medium- and heavy-duty trucks declined by approximately 4.1% compared to 2024, driven by lower new-vehicle sales. This growth trend is expected to persist throughout t...

Purchase includes:

- Report download

- Growth Dialog™ with our experts

Growth Dialog™

A tailored session with you where we identify the:- Strategic Imperatives

- Growth Opportunities

- Best Practices

- Companies to Action

Impacting your company's future growth potential.

Research Scope

The aim of this study is to research and analyze the EV charging infrastructure market in China. The market has 3 distinct segments, namely public operations (for example, at expressways, commercial areas, and neighborhood areas); dedicated operations owned by fleet companies (for example, public taxis); and private charging infrastructure that is installed and owned by EV buyers at their homes and is available for their personal use. This study presents the current scenario in the charging market in China and provides a forecast for charging points up to 2025.

Key Features

Research Objectives:

- To provide a strategic perspective of the charging market for passenger vehicles in China, including market drivers, market restraints, and SWOT analysis.

- To give an overview of government policies that affect electrification and charging solutions.

- To analyze the charging market value chain, including key market par

| Deliverable Type | Market Research |

|---|---|

| No Index | No |

| Podcast | No |

| Author | Ming Lih Chan |

| Industries | Automotive |

| WIP Number | PA68-01-00-00-00 |

| Is Prebook | No |

| GPS Codes | 9673-A6,9800-A6,9882-A6,9AF6-A6 |