USD

USD GBP

GBP CNY

CNY EUR

EUR INR

INR JPY

JPY MYR

MYR ZAR

ZAR KRW

KRW THB

THBGrowth Opportunity Assessment of Healthcare IT Market in Germany, Forecast to 2021

Growth Opportunity Assessment of Healthcare IT Market in Germany, Forecast to 2021

Healthcare IT to Help Standardize Quality of Care Across Care Settings and Regions in Germany

25-Sep-2017

Europe

Description

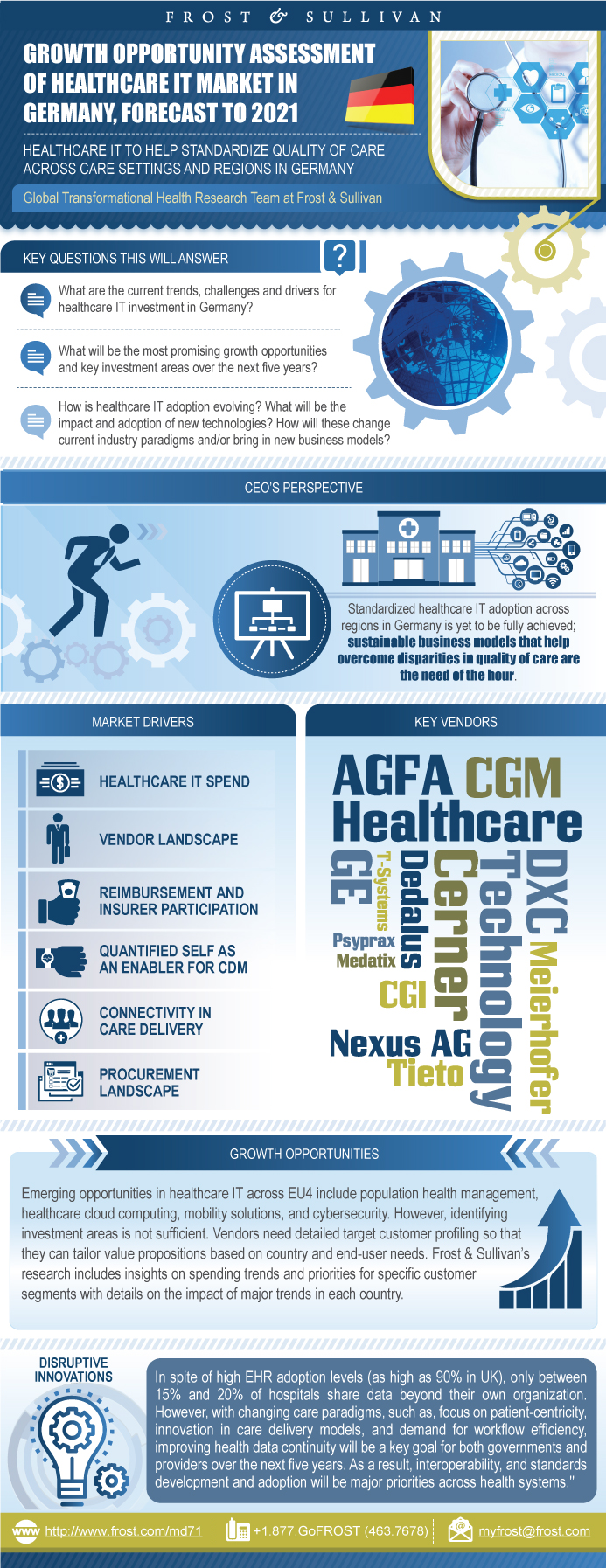

UK, Germany, France and Spain collectively spend more than $6 billion on healthcare information technology (healthcare IT), while regional adoption stands at almost 80%. Healthcare IT markets in these countries are ready to embark upon the next level of digitalization where providers move from data capturing solutions to those that can derive value from data through improving information sharing, analytics and clinical decision support.

Germany, as a country, is unique due to the early position it took towards enhancing chronic disease management in the country. As of 2017, key Growth Opportunities in the German Healthcare IT market include data sharing and interoperability solutions, cloud platforms, digital mobility, and investments in technologies that support new models of care delivery, like telehealth and telecare. However, the identification of these Growth Opportunities is only the first step towards succeeding as a vendor in this market. The real demystification lies in understanding very specific target customer needs and then building a value proposition that addresses those needs.

Between December 2016 and March 2017, Frost & Sullivan conducted a survey of IT managers from 198 hospitals across Western European countries. Findings of the survey were further investigated through in-depth discussions with market vendors and Frost & Sullivan’s industry thought leaders. Outcomes of the research have been collated into a 4-part series detailing the HCIT landscape across EU4 (the United Kingdom, Germany, France and Spain).

Our research found that despite a high level of EMR adoption, only a little more than 15% of large hospitals share data beyond their organization. This has been a huge detriment to efficient and productive health data utilization across all countries included in this study. However, with changing care paradigms, such as, focus on patient-centricity, innovation in care delivery models, and demand for workflow efficiency, improving health data continuity will be the key goal for both governments and providers over the next five years. As a result, interoperability, and standards development and adoption will be major priorities across health systems.

Overall healthcare IT market in Germany will be driven by a need for higher patient-centricity and patient engagement. German consumers are actively involved in self-management of health and wellness, not to mention chronic disease management. People in Germany are health conscious and are willing to invest in Quantified Self solutions. This consumer maturity, combined with the increasing penetration of digital and communication technologies into people’s everyday life, is driving them to demand a much greater level of healthcare knowledge and ability to action it themselves and at their convenience. As a result, over the next five years, while hospitals focus on improving the sophistication of the EMR systems, the health system as a whole will invest in patient engagement and patient experience solutions, improved data integration along the care continuum and investments in telehealth and telecare to support chronic disease management.

Vendors will have to consistently demonstrate their core competence by offering hospitals sustainable business models, centred around improved connectivity, accessibility and interoperability of healthcare. Emerging technologies, such as cloud, healthcare business intelligence and data analytics, will be in demand.

This is only a sample of insights that you can gain through our research. Key questions answered in this study include:

• What are the current trends, challenges and drivers for healthcare IT investment?

• What will be the most promising growth opportunities and key investment areas over the next five years?

• How is health IT adoption evolving?

• What will be the impact and adoption of new technologies? How will these change current industry paradigms and/or bring in new business

models?

• How are the initiatives at national and regional level for eHealth adoption impacting the market?

• What are the current vendor landscape and tiers of competition in select segments (e.g., Total Health IT, EHR, PCIS)? How are they expected to

evolve over the next five years?

• What do healthcare providers expect from vendors?

• What are the key vendor-/solution-selection criteria of providers while investing in health IT?

RESEARCH: INFOGRAPHIC

This infographic presents a brief overview of the research, and highlights the key topics discussed in it.Click image to view it in full size

Table of Contents

Research Methodology

Forecast Methodology

Market Snapshot

Scope and Segmentation

Frost & Sullivan Hospital HCIT Survey—Respondents’ Profile

Growth Opportunities in the German Healthcare IT Market

CEO’s Perspective

Market Background

Market Definition and Segmentation

Healthcare IT Market Analysis—Top 4 Markets in Europe

Macro-Level Trends Driving Care Delivery Transformation

Drivers for Healthcare IT Adoption in Germany

Healthcare IT Market Analysis––Adoption

Hospital Healthcare IT Market in Germany—Revenue Forecast

Primary Care HCIT Market in Germany—Major Trends

Overview of the Healthcare Landscape in Germany

Healthcare IT Landscape—Government Initiatives

Healthcare IT Landscape—Future Plans & Initiatives

Key Findings—Notable Vendor Activities

Key Vendors Overview—Tiers of Competition

Electronic Health Records—Market Share and Position

Primary Care Information System—Market Share and Position

ePrescribing/Pharmacy Information Systems (PhIS)—Market Share and Position

Strategic Imperatives for Healthcare IT Vendors in Germany

End-user Analysis—Adoption of Hospital HCIT Solutions

End-user Analysis—Hospital HCIT Budgeting Trends

End-user Analysis—Hospitals’ EMR Readiness

End-user Analysis—Future Trends on Replacement and Upgrades of IT Systems

End-user Analysis—Analyst Insight on Germany Hospital HCIT Market

Factors Influencing the Future of Healthcare IT in Germany

Key Conclusions and Recommendations

Legal Disclaimer

Relevant Frost & Sullivan Studies

Abbreviations and Acronyms Used

- 1. Healthcare IT Market: Top 4 Markets, Western Europe, 2016–2021

- 2. Percentage Adoption of Healthcare IT Systems, Germany, 2017

- 3. Total HCIT Market: Progression of HCIT, Germany, 2017–2020

- 1. Total Healthcare IT Market: Frost & Sullivan Research Methodology, Germany, 2017

- 2. Total Hospital HCIT Market: Frost & Sullivan Forecast Methodology, Western Europe, 2016

- 3. Total Hospital HCIT Market: Revenue Snapshot, Germany, 2016 and 2021

- 4. Total Healthcare IT Market: Leading Vendors, Germany, 2016

- 5. Total Hospital HCIT Market: Respondent’s Distribution by Region, Europe, 2017

- 6. Total Hospital HCIT Market: Respondent’s Distribution by Ownership, Germany, 2017

- 7. Total Hospital HCIT Market: Respondent’s Distribution by Specialization, Germany, 2017

- 8. Total Healthcare IT Market: Market Segmentation, Germany, 2016

- 9. Hospital HCIT Market: Revenue Forecast, Germany, 2016–2021

- 10. Healthcare System, Germany, 2017

- 11. Healthcare IT Market: Key Vendors, Germany, 2017

- 12. Healthcare IT Market: Major Vendors by Tiers of Competition, Germany, 2017

- 13. Total Healthcare IT Market: EHR Major Vendors by Tiers of Competition, Germany, 2016

- 14. Total Healthcare IT Market: EHR Market Share by Top Vendor, Germany, 2016

- 15. Total Healthcare IT Market: PCIS Major Vendors by Tiers of Competition, Germany, 2016

- 16. Total Healthcare IT Market: PCIS Market Share by Top Vendors, Germany, 2016

- 17. Total Healthcare IT Market: ePrescribing/PhIS Major Vendors by Tiers of Competition, Germany, 2016

- 18. Total Healthcare IT Market: ePrescribing/PhIS Market Share by Top Vendors, Germany, 2016

- 19. Total Hospital HCIT Market: Percentage of Budget Allocated to IT Solutions, Germany, 2017

- 20. Total Hospital HCIT Market: Percentage of Budget Increase in Last 2–3 Years, Germany, 2017

- 21. Total Hospital HCIT Market: EMR Readiness Across Hospital, Germany, 2017

Popular Topics

| No Index | No |

|---|---|

| Podcast | No |

| Table of Contents | || Research Methodology~ || Forecast Methodology~ | Executive Summary~ || Market Snapshot~ || Scope and Segmentation~ || Frost & Sullivan Hospital HCIT Survey—Respondents’ Profile~ || Growth Opportunities in the German Healthcare IT Market~ || CEO’s Perspective~ | Market Analysis of Healthcare IT in Germany~ || Market Background~ || Market Definition and Segmentation~ || Healthcare IT Market Analysis—Top 4 Markets in Europe~ || Macro-Level Trends Driving Care Delivery Transformation~ || Drivers for Healthcare IT Adoption in Germany~ || Healthcare IT Market Analysis––Adoption~ || Hospital Healthcare IT Market in Germany—Revenue Forecast~ || Primary Care HCIT Market in Germany—Major Trends~ | Government Initiatives Driving Healthcare IT Adoption in Germany~ || Overview of the Healthcare Landscape in Germany~ || Healthcare IT Landscape—Government Initiatives~ || Healthcare IT Landscape—Future Plans & Initiatives~ | Competitive Landscape~ || Key Findings—Notable Vendor Activities~ || Key Vendors Overview—Tiers of Competition~ || Electronic Health Records—Market Share and Position~ || Primary Care Information System—Market Share and Position~ || ePrescribing/Pharmacy Information Systems (PhIS)—Market Share and Position~ || Strategic Imperatives for Healthcare IT Vendors in Germany~ | End-user Analysis—Hospital HCIT Usage and Adoption Trends~ || End-user Analysis—Adoption of Hospital HCIT Solutions~ || End-user Analysis—Hospital HCIT Budgeting Trends~ || End-user Analysis—Hospitals’ EMR Readiness~ || End-user Analysis—Future Trends on Replacement and Upgrades of IT Systems~ || End-user Analysis—Analyst Insight on Germany Hospital HCIT Market~ | The Last Word~ || Factors Influencing the Future of Healthcare IT in Germany~ || Key Conclusions and Recommendations~ || Legal Disclaimer~ | Appendix~ || Relevant Frost & Sullivan Studies~ || Abbreviations and Acronyms Used~ | The Frost & Sullivan Story~ |

| List of Charts and Figures | 1. Healthcare IT Market: Top 4 Markets, Western Europe, 2016–2021~ 2. Percentage Adoption of Healthcare IT Systems, Germany, 2017~ 3. Total HCIT Market: Progression of HCIT, Germany, 2017–2020~| 1. Total Healthcare IT Market: Frost & Sullivan Research Methodology, Germany, 2017~ 2. Total Hospital HCIT Market: Frost & Sullivan Forecast Methodology, Western Europe, 2016~ 3. Total Hospital HCIT Market: Revenue Snapshot, Germany, 2016 and 2021~ 4. Total Healthcare IT Market: Leading Vendors, Germany, 2016~ 5. Total Hospital HCIT Market: Respondent’s Distribution by Region, Europe, 2017~ 6. Total Hospital HCIT Market: Respondent’s Distribution by Ownership, Germany, 2017~ 7. Total Hospital HCIT Market: Respondent’s Distribution by Specialization, Germany, 2017~ 8. Total Healthcare IT Market: Market Segmentation, Germany, 2016~ 9. Hospital HCIT Market: Revenue Forecast, Germany, 2016–2021~ 10. Healthcare System, Germany, 2017~ 11. Healthcare IT Market: Key Vendors, Germany, 2017~ 12. Healthcare IT Market: Major Vendors by Tiers of Competition, Germany, 2017~ 13. Total Healthcare IT Market: EHR Major Vendors by Tiers of Competition, Germany, 2016~ 14. Total Healthcare IT Market: EHR Market Share by Top Vendor, Germany, 2016~ 15. Total Healthcare IT Market: PCIS Major Vendors by Tiers of Competition, Germany, 2016~ 16. Total Healthcare IT Market: PCIS Market Share by Top Vendors, Germany, 2016~ 17. Total Healthcare IT Market: ePrescribing/PhIS Major Vendors by Tiers of Competition, Germany, 2016~ 18. Total Healthcare IT Market: ePrescribing/PhIS Market Share by Top Vendors, Germany, 2016~ 19. Total Hospital HCIT Market: Percentage of Budget Allocated to IT Solutions, Germany, 2017~ 20. Total Hospital HCIT Market: Percentage of Budget Increase in Last 2–3 Years, Germany, 2017~ 21. Total Hospital HCIT Market: EMR Readiness Across Hospital, Germany, 2017~ |

| Author | Shruthi Parakkal |

| Industries | Healthcare |

| WIP Number | MD71-01-00-00-00 |

| Is Prebook | No |